Market volatility returned with a vengeance during the first quarter of 2026, triggered by the joint US and Israeli strikes against Iran in late February. For months leading up to the attack, US equities had more or less traded sideways as investors attempted to price in the growing whispers of military action. On February 28th, those whispers became reality with the launch of Operation Epic Fury, sending equity markets into a sharp retreat that has yet to find a meaningful bottom.

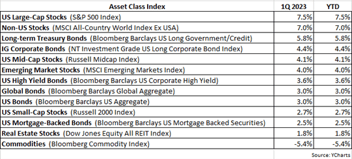

In fact, after years of being a perennial top performer, US large-cap stocks found themselves among the worst-performing asset classes in the first quarter. The S&P 500 suffered its worst start to a year since 2022, declining -4.3% — a stark reversal from the Index's dominant run.

Smaller market-cap segments of the US equity market proved more resilient. Mid- and small-cap stocks held up comparatively well, with the Russell Midcap and Russell 2000 indices posting modest gains of 1.3% and 0.9%, respectively. This relative outperformance may reflect a rotation away from the mega-cap technology names (“Magnificent 7”) that had driven large-cap indices to extremely stretched valuations, as investors reassessed growth expectations in a more uncertain interest rate environment.

As for non-US equities, the MSCI All-Country World Index ex-USA surged nearly 11% through mid-quarter, fueled by a weakening US dollar and renewed investor interest in European and emerging market stocks. However, that impressive rally was swiftly reversed following the escalation of tensions in the Middle East. The Iranian strike introduced a fresh wave of geopolitical risk, triggering a broad risk-off move that erased virtually all of the quarter's gains, and then some, by the time March came to a close.

Fixed-income markets followed a similar trajectory to equities during the quarter. Most bond categories rallied steadily through January and February, buoyed by moderating inflation data and growing expectations that the Federal Reserve was nearing the end of its tightening cycle, only to abruptly reverse course in the wake of the Iranian strike. The same geopolitical shock that rattled equity markets sent bond investors scrambling as well. Prior to the attack, interest rates had been on a sustained downward trend, providing a favorable tailwind for fixed income across virtually all categories. But that constructive backdrop changed almost overnight. With the closure of the Strait of Hormuz sending crude oil prices sharply higher, inflation concerns that had been gradually fading roared back to the forefront. Rising energy costs forced investors to quickly recalibrate their interest rate expectations accordingly, sending yields higher and bond prices lower.

As of this writing, it remains unclear when, or whether, the Strait of Hormuz will finally reopen. The stakes are considerable: the strait serves as one of the world's most critical chokepoints for global energy supply, with an estimated 20% of all oil traded globally passing through it on any given day. A prolonged closure would likely sustain upward pressure on energy prices well beyond what markets have already priced in, with ripple effects felt across nearly every corner of the global economy.

Such a predicament would leave the Fed Reserve in a familiar but uncomfortable position. Historically, the Fed has tended to look through energy price spikes driven by geopolitical events, treating them as temporary supply disruptions unlikely to warrant a fundamental shift in monetary policy. The logic is straightforward: hiking rates to combat inflation caused by a supply shock, rather than excess demand, risks inflicting unnecessary economic pain without addressing the root cause.

In this instance, however, the calculus may be more complicated. Inflation, while declining from its post-pandemic peaks, has proven stickier than many had hoped, and the Fed's credibility on price stability remains a primary concern. If the Strait remains closed for an extended period and energy prices stay elevated, pressure on the Fed to act — even in the face of a geopolitically-driven shock — could mount quickly. Whether policymakers once again treat this as a transitory event or feel compelled to respond more forcefully will likely be one of the defining questions for both bond and equity markets in the quarters ahead.

Among all asset classes, commodities were the standout winners of the first quarter. Crude oil (WTI) led the charge surging 77% as the closure of the Strait of Hormuz effectively removed roughly 20% of global oil supply from the market almost instantaneously. When a single geopolitical event can sever one of the world's most critical energy arteries overnight, the price response, no matter how dramatic, is not entirely surprising. Precious metals also posted gains on the quarter, with gold rising about 8%.

On the surface, this price rise seems consistent with gold's historical reputation as a safe-haven asset — a reliable store of value during periods of uncertainty, conflict, and market stress. Yet what has many investors perplexed is how gold has performed during this Iran war. Since the conflict began at the end of February, gold has declined approximately -11%, a striking divergence from what one would expect of the world's preeminent crisis hedging vehicle during an active military event. In response to this atypical price behavior, it’s not unreasonable to ask: why is the price of gold falling when by precedent it should be rising, or at the very least holding its ground?

The answer to this question appears to be directly tied to the very same forces driving up the price of oil. Unlike the US — which has become a net exporter of oil due to the fracking/shale revolution — the majority of the world's largest economies are heavily dependent on imported oil. China, India, Japan, South Korea, and most of the Eurozone collectively account for as much as 70% of global crude oil demand. With oil prices recently having surged more than 70%, these nations are now facing dramatically higher energy bills, and those bills must be paid in US dollars, the currency in which crude oil is exclusively traded globally.

To meet this sudden and steep increase in dollar-denominated energy costs, many of these countries' central banks have turned to one of their most liquid and universally accepted assets: gold. By selling gold reserves on the open market and converting the proceeds into dollars, these institutions can fund their oil purchases without depleting foreign currency reserves or resorting to more disruptive measures. The result is a significant and sustained wave of central bank gold selling — selling that is overwhelming the safe-haven buying one might otherwise expect in a time of geopolitical crisis, and putting meaningful downward pressure on the precious metal's price.

It is, in a sense, an ironic feedback loop: the same war driving oil prices to extraordinary heights is simultaneously suppressing gold, an asset that, under any other set of circumstances, would likely be surging alongside it. Whether this dynamic persists will depend largely on how long the Strait of Hormuz remains closed and how aggressively central banks continue to draw down their gold reserves to manage the energy shock. For now, it serves as a reminder that in complex, interconnected global markets, even the most time-tested relationships can break down in unexpected ways.

As for how the repercussions of this war could affect the US economy and markets more broadly, it is still too early to draw any firm conclusions. Wars and geopolitical crises have a way of evolving in unpredictable directions, and history cautions against making premature sweeping pronouncements or trying to second-guess every new development while the situation remains fluid. Energy costs are the most immediate and visible pressure point. Gasoline prices have already climbed sharply at the pump, functioning as an effective tax on consumers and businesses alike, one that if sustained has the potential to meaningfully weigh on consumer spending, squeeze corporate margins, and slow overall economic momentum. The US economy has demonstrated remarkable resilience in recent years, but a prolonged period of elevated energy prices would test that resilience in ways that are difficult to fully anticipate.

Consumer confidence is also sensitive to geopolitical stress, and a prolonged conflict with no clear end in sight could gradually erode the spending optimism that has been a key pillar of economic strength in recent quarters. It’s always worth reminding that the US economy is, at its core, a consumer-driven machine. Household spending accounts for roughly 70% of GDP — a share that dwarfs every other component of economic activity, including business investment, government spending, and net exports combined. If elevated energy prices begin to materially crimp household budgets, the ripple effects through the broader economy could be significant and self-reinforcing. Higher energy costs leave consumers with less discretionary income to spend on everything else. Businesses, sensing a pullback in demand, may respond by slowing hiring or investment, which in turn weighs further on consumer confidence and spending. It is a feedback loop that, once set in motion, can be difficult to reverse. In short, what happens at the gas pump over the coming months may prove to be one of the most important variables in determining the health of the US economy for the remainder of the year.

Perhaps the greatest unknown is how long this conflict endures and whether or not it remains contained within the region. A swift resolution that reopens the Strait of Hormuz and restores normal oil flows would likely allow markets to recover much of the ground lost, with limited long-term economic damage. On the other hand, a protracted, metastasizing war would present a far more serious and complex challenge, both for the global economy and for a Fed already navigating a delicate policy environment.

We are monitoring developments closely and will continue to share our perspective as the situation evolves. In the meantime, we believe it is especially important to resist the temptation to make dramatic portfolio changes in response to short-term uncertainty. The instinct to act decisively in moments of stress is understandable, but it has historically been one of the more reliable ways investors undermine their own long-term outcomes. Instead, we remain anchored to the disciplined, long-term investment process that has guided our approach over the years.

We’ll conclude by saying what we’ve been saying for the last few quarters. With respect to client portfolios, we remain defensively positioned as we are always being as mindful and vigilant about preserving capital as we are about striving to achieve significant relative performance gains.

If you have any questions, please feel free to call or email.

As always, the entire team at Measured Wealth wishes to thank you for entrusting us to deliver on your financial goals.

Edward Miller, CFA, CMT

%20(2).png?width=1200&height=400&name=Edward%20Miller%2c%20CFA%2c%20CMT%20Chief%20Investment%20Officer%20Measured%20Wealth%20Private%20Client%20Group%20(1200%20x%20400%20px)%20(2).png)

Important Disclosures

Historical data is not a guarantee that any of the events described will occur or that any strategy will be successful. Past performance is not indicative of future results.

Returns citied above are from various sources including Factset, Bloomberg, Russell Associates, S&P Dow Jones, MSCI Inc., The St. Louis Federal Reserve and Y-Charts, Inc. The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security. Investing involves risks, including possible loss of principal. Please consider the investment objectives, risks, charges, and expenses of any security carefully before investing.

“ ’Magnificent 7’ is a market term and is being used for illustrative purposes only. The individual securities and related returns shown are presented solely for illustrative and informational purposes to demonstrate recent market trends. They are not intended to represent holdings in any Measured Wealth portfolio, nor do they represent investment recommendations or past or current performance of any Measured Wealth strategy. Measured Wealth may or may not hold any of the securities discussed.”

In order to provide effective management of your account, it is important that we have current information regarding your financial status and circumstances. Please contact us in writing at 303 Islington Street, Portsmouth, NH 03801 if you have any changes in your financial situation or investment objectives, and whether you wish to impose any reasonable restrictions on the management of the account or reasonably modify existing restrictions.

Measured Wealth Private Client Group, LLC is an investment adviser located in Portsmouth, New Hampshire. Measured Wealth Private Client Group, LLC is registered with the Securities and Exchange Commission (SEC). Registration of an investment adviser does not imply any specific level of skill or training and does not constitute an endorsement of the firm by the Commission. Measured Wealth Private Client Group, LLC only transacts business in states in which it is properly registered or is excluded or exempted from registration.

This publication is provided to clients and prospective clients of Measured Wealth Private Client Group, LLC for general informational and educational purposes only. It does not: (i) consider any person's individual needs, objectives, or circumstances; (ii) contain a recommendation, offer, or solicitation to buy or sell securities, or to enter into an agreement for investment advisory services; or (iii) constitute investment advice on which any person should or may rely. Mention of any particular security in this publication, including reference to the performance of a particular security, is for illustrative purposes only. Clients of Measured Wealth may hold positions in the security, and Measured Wealth may buy or sell the security at any time. Past performance is no indication of future investment results. This publication is based on information obtained from third parties. While Measured Wealth Private Client Group, LLC seeks information from sources it believes to be reliable, Measured Wealth Private Client Group, LLC has not verified, and cannot guarantee the accuracy, timeliness, or completeness, of the third-party information used in preparing this publication. The third-party information and this publication are provided on an “as is” basis without warranty.

This publication may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “should,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio's operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Measured Wealth Private Client Group, LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.