Market Recap

Last month, stocks picked up where they left off in April. The S&P 500 rose 5.3% in May, adding further gains to what had already been its best month since November 2020. Emerging markets led all major indices with a gain of 9.7% as non-US equities continue to demonstrate that last year's stellar gains were likely not a flash in the pan — though it remains uncertain whether this trend will persist. Through the end of May, the S&P 500 is up 11.3% year-to-date (YTD), while the NASDAQ has surged 16.3% and the Russell 2000 Index has posted an impressive 18.2% gain YTD. It's encouraging to see the market's advance continuing to broaden beyond mega-cap names, with mid- and smaller-cap stocks increasingly participating in the rally.

On the sector front, technology was the standout performer. The Technology SPDR ETF (XLK) posted a gain of nearly 20% in May alone — a figure that would be noteworthy for a full calendar year, let alone a single month. The next best-performing sector, health care, rose just 2.4% by comparison, underscoring just how dominant technology's return was in the month. At the other end of the spectrum, energy was the weakest performer, suggesting that investors may be rotating out of a sector that — despite last month's softness — remains up nearly 27% for the year.

Corporate earnings continue to provide a solid fundamental backdrop. More than 80% of S&P 500 companies reporting first-quarter 2026 results have beaten analyst estimates. Looking ahead, Wall Street analysts are projecting full-year 2026 earnings growth of approximately 21% — an ambitious target we believe will require continued execution from companies to justify current high valuations.

Federal Reserve

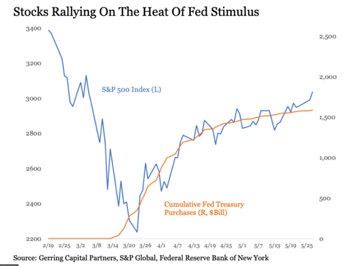

May also marked a long-anticipated transition at the Federal Reserve, as Kevin Warsh officially took the helm as Chair, succeeding Jerome Powell. Warsh arrives with a well-established reputation as an inflation hawk — someone inclined to favor higher interest rates to subdue rising prices. At the same time, President Trump has been vocal in his desire to see the Fed cut rates, and it is reasonable to assume he expects his nominee to be receptive to that pressure.

Of course, the Fed is intended to operate as an independent institution, insulated from political influence. How Warsh chooses to navigate the tension between his own policy instincts, the administration's expectations, and the Fed's institutional mandate will likely be one of the more interesting subplots to track over the months ahead.

A Note on Our Positioning

It has come to my attention that my prior investment letters over the last several months have been decidedly bearish or negative. Upon reflection, that characterization is likely accurate — though I would gently push back on the word "bearish" in favor of "cautiously optimistic." A few points of clarification seem worth discussing.

First, when I've stated that "client portfolios remain defensively oriented," such positioning does not mean all positions in a client portfolio are inherently defensive. Rather, I mean that the portfolio model as a whole — encompassing both defensive and more growth-oriented positions — tilts, on a net basis, toward capital preservation over aggressively seeking capital gains. Portfolio positioning will also vary by client based on individual objectives, risk tolerance, and account constraints.

Second, at Measured Wealth, the concept of being "defensive" is relative, not absolute. Our benchmark of comparison is typically a broad market index such as the S&P 500. To illustrate: if a defensive sector like health care represents 12% of the S&P 500, a defensively oriented portfolio would overweight that sector, holding more than 12%. Conversely, if a more aggressive, risk-on sector like technology carries a 30% weight in the Index, a defensive posture would mean underweighting that sector, holding less than 30%. It is this relative positioning that defines our current stance — not the wholesale abandonment of growth-oriented investments.

Lastly, the primary reason for our defensive positioning over the past several months has been the persistent bearish signals flashing across many of the indicators we closely follow. Historically, these indicators have been associated with market turning points, yet this market cycle has proven to be a perplexing exception.

This Time It's Different?

Since the COVID-driven market collapse of 2020, the word "unprecedented" has become almost a permanent fixture in the financial lexicon. The traditional relationships between economic data, monetary policy, and market behavior that guided investors for decades have repeatedly broken down or behaved in ways few could have anticipated. Correlations that once held firm have inverted. Recoveries that should have taken years unfolded in months. Markets have shrugged off conditions that, in any prior cycle, would likely have led to prolonged downturns.

We believe this does not mean our indicators are broken — but rather that the environment in which they operate has been fundamentally altered by extraordinary levels of fiscal and monetary intervention, structural shifts in market participation, and a macro backdrop unlike anything in modern financial history. As always, we remain disciplined in our process while acknowledging the possibility that this cycle may continue to write its own rules. It's rarely ever true, but perhaps the oft-dismissed phrase "this time it's different" might actually have some validity.

Looking Ahead to June

We enter June with three major themes on our radar:

1. Inflation & Fed Policy. The trajectory of inflation and what it means for the Fed's first real policy decision under Warsh will be closely watched.

2. Technology & AI Earnings. The durability of technology and AI-driven earnings growth that has powered this rally remains a key question as we move into the second half of the year.

3. Geopolitical & Energy. Developments in energy markets have kept oil prices elevated and created a meaningful drag on consumer spending — a situation we continue to monitor closely.

As always, please do not hesitate to reach out if you have questions about your specific portfolio, your financial plan, or anything you have read here. The entire team at Measured Wealth wishes to thank you for the opportunity to assist you through your financial journey.

Important Disclosures

The views expressed herein, including those of guests not affiliated with Measured Wealth, reflect the opinions of the author as of the date of publication and are subject to change without notice. This communication is provided for informational and educational purposes only, does not constitute investment, tax, or legal advice. Any references to specific securities, products, or services do not constitute a recommendation or endorsement. All forward-looking statements and projections are subject to uncertainty and should not be relied upon as predictions of future results. All investments involve risk, including the possible loss of principal. Past performance of any security, index, strategy, or market is not indicative of future results. Any index performance referenced herein is provided for informational context only; indices are unmanaged, do not incur fees, and are not available for direct investment. Statistical data attributed to third parties is believed to be from reliable sources but has not been independently verified.

Source

Source: Market data referenced above was obtained from Y-Charts and Stockcharts.com and is provided for informational purposes only.